-

For banks with assets between $10 billion and $100 billion, the average exposure is 165% of capital.

June 24

-

The firm also predicts that the coronavirus pandemic will delay the GSEs' release from government control.

June 3

-

The ratings firm also took negative action with respect to Ally, Synchrony, Discover, Sallie Mae and Navient, citing the impact that the coronavirus crisis is having on their revenues and profits.

April 29

-

According to a new academic research report, CLO managers have taken advantage of S&P's ratings methodology for a ratings boost on lower-rated tranches - enabling them to offer more return for what seemed like less risk.

April 21

-

Fitch assumes a significant spike in defaults over the next few months, as well as declining new issuance volume during the second and third quarters of 2020, fewer maturing loans and fewer resolutions by special servicers.

April 9

-

Historically low interest rates, low unemployment and positive yet slowing economic growth will support stable U.S. structured finance asset performance in 2020.

January 28

-

The delinquency rate for commercial mortgage-backed securities ended 2019 at its lowest point in nearly 11 years, aided by increased issuance and the resolution of legacy transactions, Fitch Ratings said.

January 10

-

Charge-offs in prime bank cards fell to 3.01%, a third consecutive month in the sector. Meanwhile, retail-card ABS had its best charge-off performance since October 2018.

September 5

- LIBOR

Trustees are concerned about obtaining proper consents from legacy residential mortgage-backed securities investors in a timely fashion in order to make the switch from Libor to another index, Fitch Ratings said.

August 21

-

Life insurance companies increased their mortgage investments to levels higher than historical norms, creating more potential danger for their portfolios in the event of a real estate downturn, a Fitch Ratings report said.

July 15

-

The post-crisis operational improvements at both Fannie Mae and Freddie Mac have resulted in stronger mortgage loan performance, a Fitch Ratings report said.

July 3

-

Mortgages using alternative documentation like bank statements for underwriting performed stronger than expected, but uncertainty remains about their default rates in stressed environments, Fitch Ratings said.

July 2

-

Revisions to S&P's CLO ratings methadology and Kroll's launch into rating European CLOs could challenge Moody's as the first choice for managers across the pond.

June 25

-

The two agencies offer fundamentally different views of the level of risk in ABS issuances by Avant, Prosper Marketplace, LendingClub and other online lenders.

May 27

-

Delinquencies associated with the government-sponsored enterprises high loan-to-value ratio programs that target low-to-moderate income homebuyers are slightly better than expected, at least early on, according to Fitch.

May 23

-

Private-label mortgage securitizations with variable servicing fee arrangements could become more common going forward as issuers look to increase investor cash flow while reducing the loan servicer's economic exposure, Fitch said.

May 6

-

Commercial mortgages placed into special servicing grew last year, but default and foreclosure dollar volume fell as legacy loan resolutions outpaced newly distressed loans, according to Fitch Ratings.

April 29

-

The rating agency has developed rating criteria for bonds backed by oil and gas royalties, though such deals would be capped at the 'A' rating category.

February 14

-

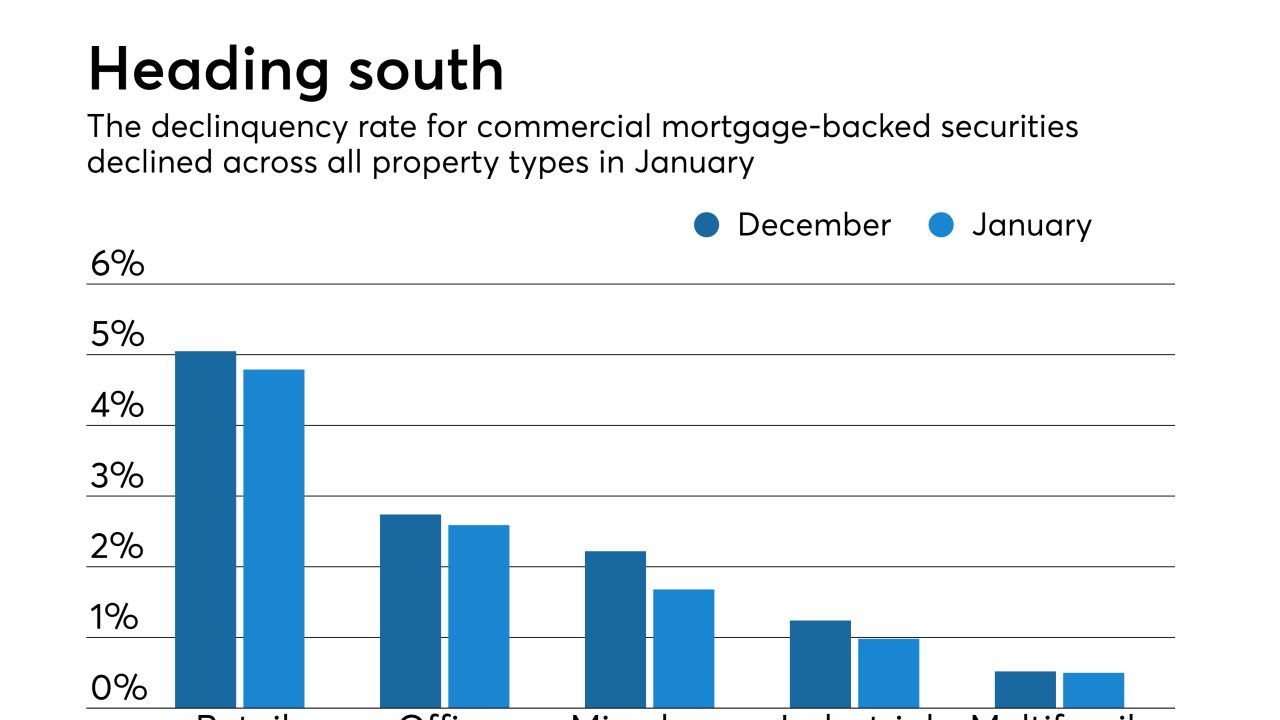

Late payments on loans backing commercial mortgage bonds continued falling at the start of the year, due to strong new issuance volume and continued resolutions for precrisis loans by special servicers, according to Fitch Ratings.

February 11

-

Loans in commercial mortgage-backed securities originated after 2009 by nonbank lenders have a significantly higher default rate than those originated by banks, a Fitch Ratings report said.

January 14