The $770 million transaction is also more concentrated in terms of obligors than MassMutual's prior deal, though more of these corporate obligors have investment-grade ratings, resulting in a lower WARF.

-

The concentration of loans with terms of 73-75 months has breached 13%, after ranging from between 10-12% from five previous AART issues since 2016.

June 18

-

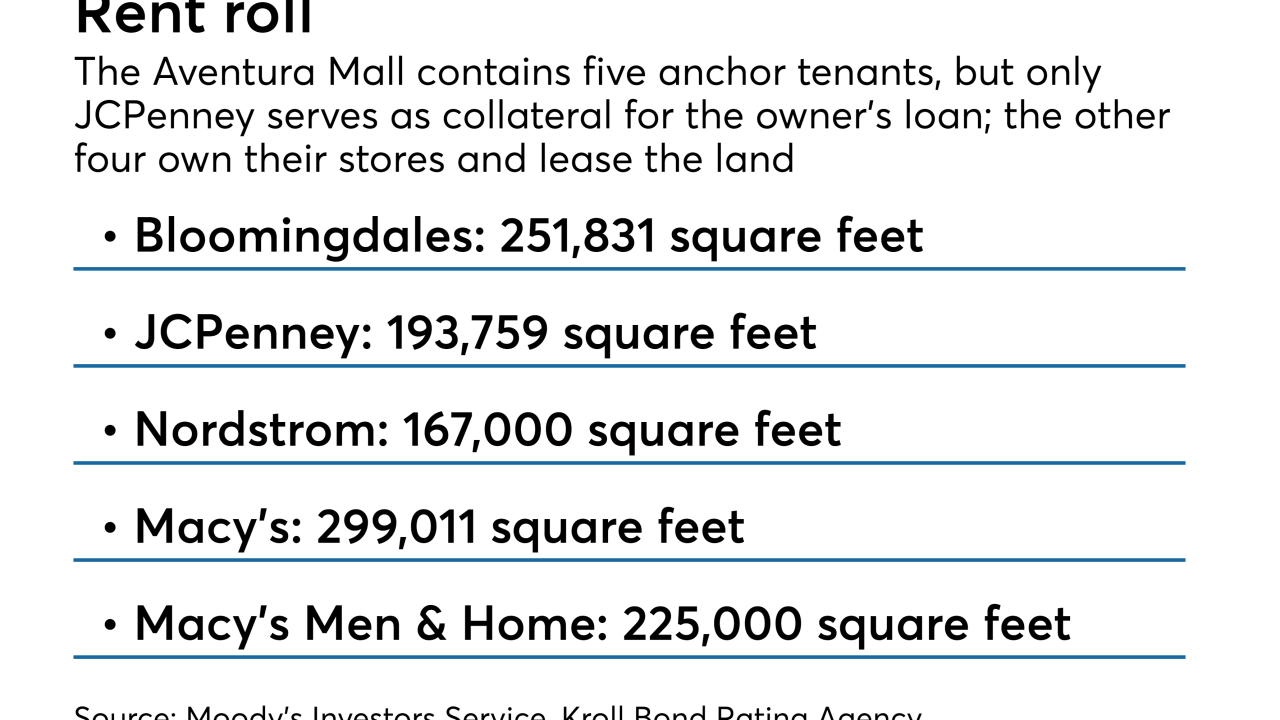

The 10-year, fixed-rate term of the $1.75 billion interest-only loan may raise some eyebrows, though the owners still have "implied equity" of $1.7 billion in the 2.2 million square foot property, per Moody's Investors Service.

June 18

June 18

-

Risk management and technology systems at the Federal Housing Administration lag decades behind Fannie Mae and Freddie Mac and desperately need to be revamped, according to a top official at HUD.

June 18

-

New securitizations backed by reverse mortgages are now at a low not seen in two years, signaling that higher volumes seen in recent months may be tapering off.

June 18

June 18

-

Like the sponsor's February transaction, this one is backed by midsize and larger business jets, a volatile asset class; it amortizes more slowly and has looser restrictions on extending the terms of leases and loans.

June 18

-

The $100 million Series 2018-1 notes will rank on an equal basis with the $900 million of notes Coinstar issued from the same master trust in May 2017, all are collateralized by nearly 20,000 coin-counting kiosks located in major retail stores.

June 15

-

In Santander Consumer USA's third subprime shelf offering of 2018, new cars represent 55.8% of the collateral. In previous deals dating to 2013 new-car concentrations did not exceed 40.9%.

June 15

-

The borrowers in the pool of collateral have lower FICO scores, and the size of a prefunding account has risen to 25% of the initial balance from 16% for Marriott's prior deal, completed in August 2017.

June 15

-

Five classes of notes will be issued in the transaction, BBVA Consumer Auto 2018-1, which is backed by a pool of well-seasoned loans on new and used cars that will revolve for an initial period of 1.5 years.

June 14

-

CLO securities pay out interest pegged to the three-month London interbank offered rate, but loans used as collateral are increasingly switching to one-month Libor and the spread between the two benchmarks has widened significantly.

June 14

-

The $278.3 million RCMF 2018-FL2 also has unusually heavy exposure to apartment buildings, offices and industrial properties that are either vacant or have low occupancy levels, according to Kroll Bond Rating Agency.

June 14

-

The average FICO for the pool of lease obligors is at a peak level for GM Financial's shelf, but Fitch expects higher losses on resale values on a pool more heavily dependent on longer-term leases and luxury models.

June 14