-

The Structured Finance Association questions whether funding closed-end seconds is an appropriate role for the government-sponsored enterprise, while newer lenders welcome the liquidity support.

April 17

April 17

-

The bank is a top auto lender, with a managed portfolio of $7.1 million through December 2023, and has a strong servicing track record.

April 17

-

The initial protection amount, Moody's says, is 12.5% of the total reference pool and equals the principal amount of the rated and unrated issued notes.

April 17

-

ADMT 2024-NQM2 will repay senior position investors on a pro-rata basis, while the mezzanine and subordinate notes will be repaid sequentially.

April 16

-

That the underlying contract holders prioritize using their smartphones and other mobile devices suggests that they are likely to prioritize payments related to those products.

April 15

-

Chris Hentemann, whose fund manages $6.2 billion in assets, seeks out B-piece opportunities and foresees banks executing more bulk loan sales and credit-risk transfers.

April 15

-

The current levels of credit enhancement are a reduction from levels of 58.0%, 48.7%, 35.9%, 22.5% and 17% on the classes A, B, C, D and E on the BLAST 2024-1 deal.

April 12

-

The financing outlook improved from recent surveys on a macro basis, but expectations around commercial real estate helped cloud over the credit forecast.

April 12

-

Fiber securitization backed by month-to-month residential fiber internet revenue didn't exist before 2022. Before that, there were some smaller transactions secured by long-term contracts.

April 12

-

Most of the notes will be fixed rate, but the A1B tranche could be benchmarked to the three-month Secured Overnight Financing Rate (SOFR).

April 11

-

Griffin was a managing director at J.P.Morgan Securities, where he ran the global primary collateralized loan obligation (CLO) business.

April 11 -

A pool of open-end vehicle fleet lease and loan contracts for cars, trucks and other vehicles provide the revenues to the bonds.

April 11

-

There are four risk events that could stop cash flow into SMB 2024-R1's deal—missing overcollateralization targets, a stymied principal distribution and the deals do not exercise an optional clean-up call.

April 10

-

Wednesday's report adds to evidence that progress on taming inflation may be stalling, despite the Fed keeping interest rates at a two-decade high.

April 10

-

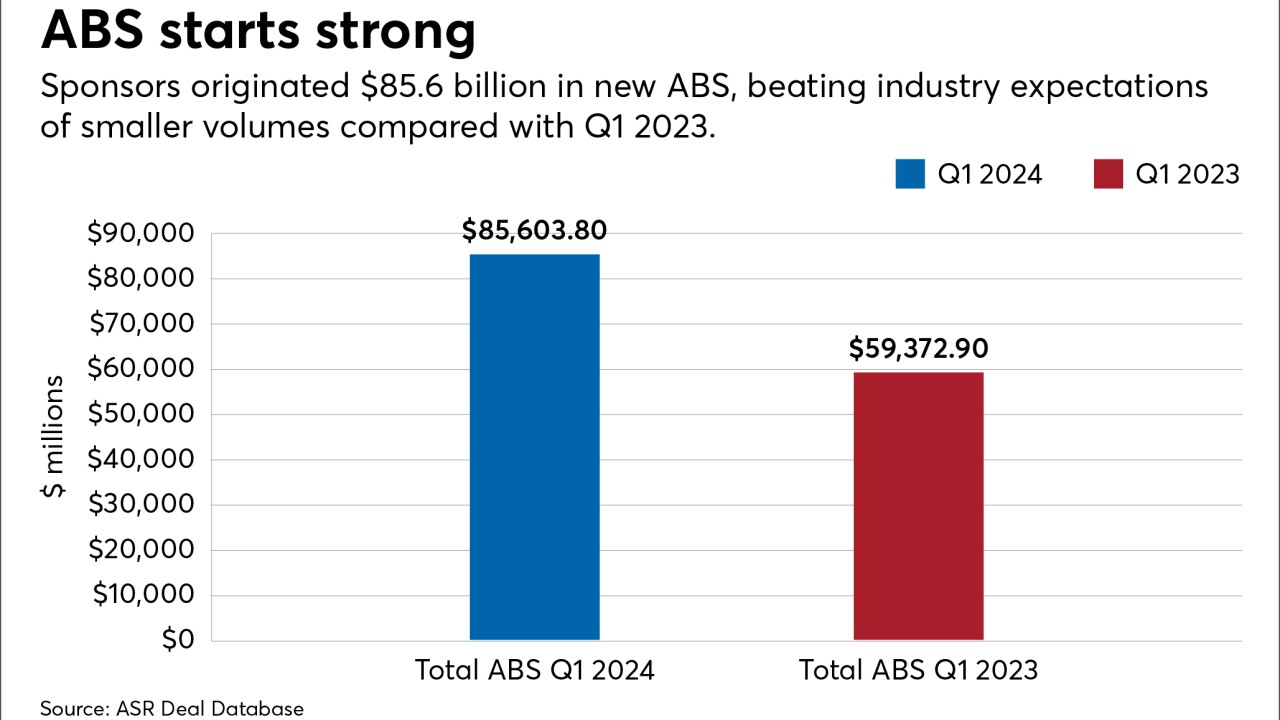

New originations exceeded last year's tally by 30.5%, despite concerns about how rates might impact consumer financial strength. Auto ABS production revved up overall performance.

April 9

-

Aside from overcollateralization and subordination, the notes get support from a reserve account representing 0.96% of the pool and an incremental reserve account maintain 1.00%.

April 9

-

Biden's "Plan B" would see loans reduced or wiped out for millions of Americans — including those whose debt exceeds their original principal amount.

April 8

-

Series 2024-2 can be upsized to $1.5 billion from the base pool amount, but regardless of the increase, pricing guidance, total credit enhancements and legal final maturities are expected to remain the same.

April 8

-

At the pool level, loans have a weighted average minimum liquid reserve of $5 million, and at the loan level the minimum for liquid reserves is $1 million for sponsors without a FICO score.

April 5

-

BJETS 2024-1 has leases and loans on 31 business jets in the collateral pool, 12 from Gulfstream and 11 from Bombardier, the two largest contributors.

April 4