-

The structure includes a stop-advance feature, which will prevent the servicer from providing scheduled interest and principal on loans that are 120 days or more delinquent.

6h ago

6h ago

-

Assets have a non-zero credit score is 631, notably lower than previous transactions. Also, a slight majority of borrowers, 53.23%, have credit scores of 660 or lower.

August 6

-

The current pool's major loan characteristics were higher than that those seen on the RKTL 2026-2, with 60-month loans representing a higher concentration of the current pool (77.0%) compared with 73.7% on the previous deal.

August 5

-

The aircraft assets will be prefunded, otherwise, the proceeds will refinance 15 vintage aircraft.

August 5

-

Interest will be repaid sequentially. Scheduled principal will be paid based on the scheduled outstanding note balance for the applicable payment period and the note balances.

August 4

-

The group is planting a flag for a new structured finance platform and real estate finance team in Miami and is expected to also strengthen Benesch's New York presence with two partners.

August 4

-

Notes are expected to pay coupons of 5.69% on the A1A notes and 5.89% on the A1B notes. Beyond that, the A2 and A3 notes pay coupons of 5.92% and 5.97%, respectively.

August 3

-

Structured as a master trust deal, AVCCT 2026-1 includes a three-year revolving period, when no principal payments will be made on the series 2026-1—unless an early amortization event happens.

July 31

-

Notes are expected to pay coupons of 4.05% on the notes rated R-1 (high) (sf) and 4.59% and 4.79% on the A1 and A2 notes, respectively.

July 29

-

A mix of underwriting methods were used on the asset pool, but alternative documentation took a larger portion than the rest, accounting for 35.5%.

July 28

-

The RMBS deal expects to pay coupons of 4.53% on the A1A through B4 notes, virtually all the notes in the capital structure.

July 27

-

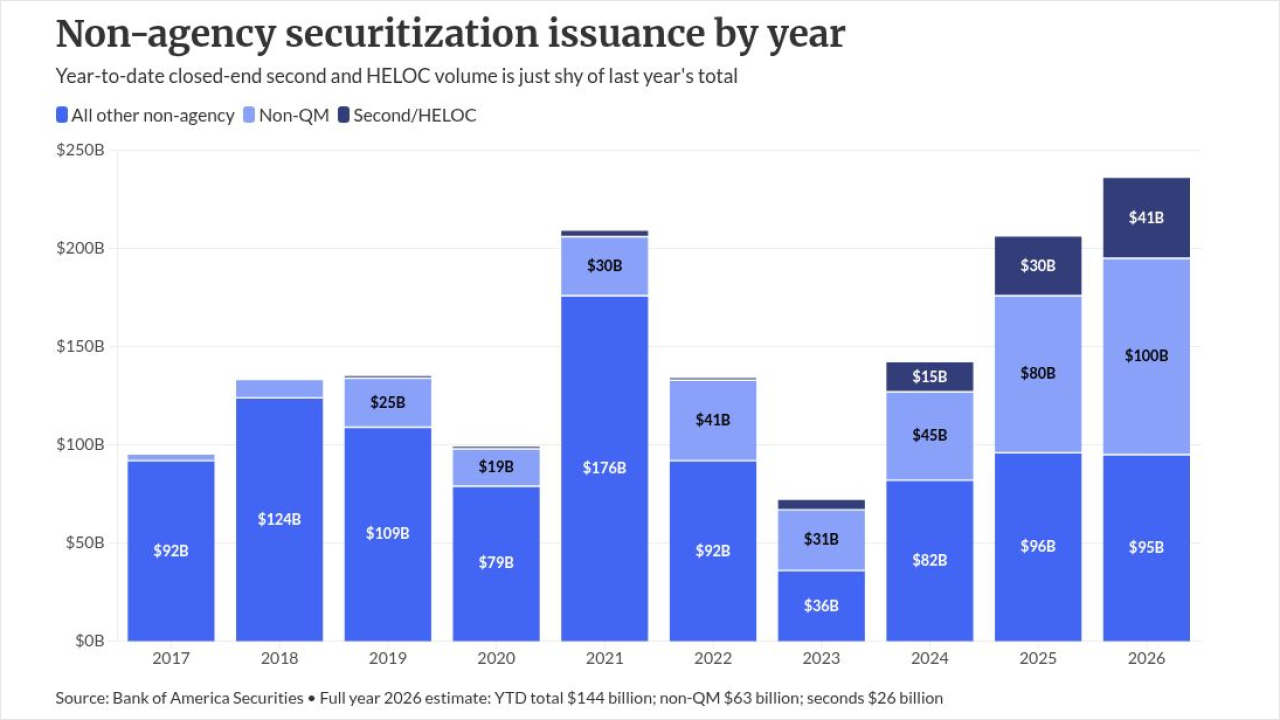

So far this year, the volume of closed-end second and home equity line of credit securitizations is near last year's $29 billion, Bank of America Securities said.

July 27

July 27

-

Equipment loans and leases that Redaptive Sustainability primarily acquired from originators, will back the asset pool.

July 24

-

Shareholders of XAI Floating Rate & Alternative Income should not support Octagon's removal as the fund's sub-adviser, Egan-Jones said, citing limited benefits to shareholders.

July 24

-

The rule 144A deal's structure includes a cash collateral account represents 1.00% of the note balance across all tranches.

July 23

-

The transaction will repay senior fees, principal and interest on the A1 class before repaying monthly interest on all remaining outstanding classes of notes.

July 22 -

CIP, which specializes in energy infrastructure, is working with Morgan Stanley on a collateralized fund obligation. The transaction could be around $1 billion.

July 22

-

Almost one third of borrowers in the pool, 26.3%, are self-employed, with a non-zero weighted average (WA) average income of $832,522, and $666,211 in liquid reserves.

July 21

-

The top 20 obligors account for 32.0% of the aggregate securitization value, while the top 10 represent 18.8%, a moderately elevated concentration.

July 21

-

Servicers of ACHM Trust 2026-HE1's underlying mortgages are also not required to forward any principal and interest advances on the mortgage loans they service.

July 21