-

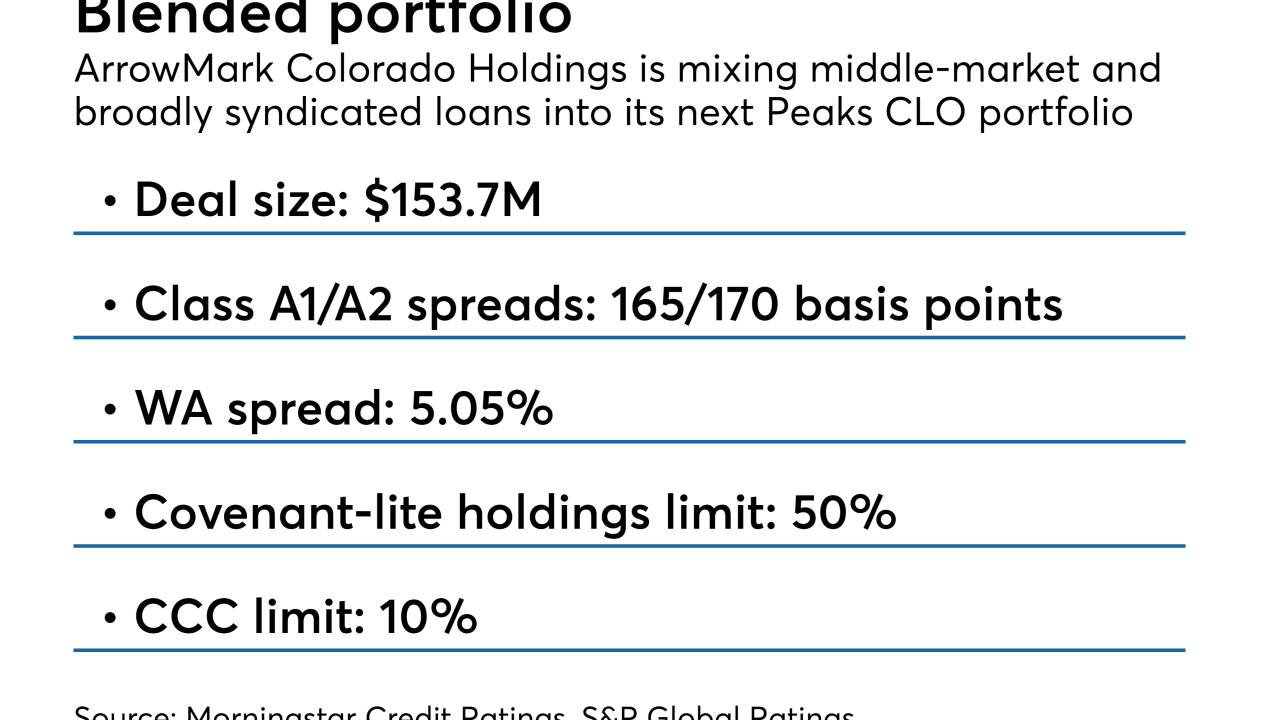

The $153.7 million Peaks CLO 3 also features a high ceiling for triple-C-rated loans and for "current-pay" loans that meet one or more criteria for default.

December 10

-

New Penn Financial will change its name to NewRez at the start of 2019, reflecting its acquisition earlier this year by New Residential Investment Corp.

December 7

December 7

-

FORT CRE 2018-1 will include four loans recycled from the prior deal, including one that Kroll has identified as a loan of concern due to weak operating performance.

December 5

December 5

-

The sponsor appears to be paying for the privilege; the deal is structured with a super senior tranche of notes that benefits from considerably more subordination than the senior tranche of its prior deal.

December 4

-

Consolidation is coming in the mortgage industry, but a protracted timetable will continue to constrict industry profits.

December 4

December 4

-

Both managers are pricing their 3rd CLOs of 2018; the 135 basis point spread on Zais' is among the widest this year for a deal backed by broadly syndicated loans.

November 27

-

The pool includes loans for 23 new construction, converted or acquired assets, each in a pre-stabilization phase awaiting refinancing through a permanent agency takeout loan.

November 21

-

Guggenheim joins GSO/Blackstone and Bain Capital as longtime CLO managers expanding into the SME space this year.

November 21

-

We are one year deeper into an already extended credit cycle, so it’s even more important to focus on market complacency.

November 20 Fitch Ratings

Fitch Ratings -

More collateralized loan obligations are failing weighted-average lift tests due to the dearth of available loans whose near-term maturities could provide some relief to portfolios.

November 20

-

Chicago officials say the city will complete its $3 billion securitization program with a $600 million deal as soon as January.

November 19

November 19

-

Eagle Point's CEO criticized "hyperbole" about growing risks in leveraged loans and CLOs, noting the benefits that price volatility can present to equity buyers.

November 15

-

The structured credit specialist will more than double its $2.9 billion in assets by acquiring a portfolio of three collateralized loan obligations that Trimaran Advisors runs from KCAP Financial.

November 12

-

The $600 million FORT CRE 2018-1 is more highly leveraged than the private equity group's debut transaction in August 2016, it is also actively managed and includes a $50 million tranche of revolving notes.

November 12

-

Continued diversification of its business lines and better margins in its securitization activities helped Redwood Trust overcome steep mortgage origination declines and post nearly 14% annual growth in net income during the third quarter.

November 8

November 8

-

According to presale reports, PGIM is marketing a $509.5 million Dryden 61 CLO transaction in the states, while also prepping a €411 million Dryden 66 Euro CLO portfolio.

November 6 -

The transaction is one of only three CRE CLOs issued post crises with a collateral balance of $1.0 billion or more, according to Kroll Bond Rating Agency.

November 5

-

The unique approach Fannie Mae and Freddie Mac are each taking with their credit-risk transfer products is quickly becoming a key point of differentiation that's rekindling competition between the government-sponsored enterprises.

November 2

-

Laurel Davis, VP, credit risk transfer at Fannie Mae, explains why the switch to a REMIC structure for CAS is important, and why it took so long.

November 2

-

The company’s first transaction, Eagle Re 2018-1, transfers a portion of the credit risk on approximately $36.3 billion of mortgages, according to Morningstar Credit Ratings.

November 2