-

Most of the notes will be fixed rate, but the A1B tranche could be benchmarked to the three-month Secured Overnight Financing Rate (SOFR).

April 11

April 11

-

Griffin was a managing director at J.P.Morgan Securities, where he ran the global primary collateralized loan obligation (CLO) business.

April 11 -

A pool of open-end vehicle fleet lease and loan contracts for cars, trucks and other vehicles provide the revenues to the bonds.

April 11

-

There are four risk events that could stop cash flow into SMB 2024-R1's deal—missing overcollateralization targets, a stymied principal distribution and the deals do not exercise an optional clean-up call.

April 10

-

Wednesday's report adds to evidence that progress on taming inflation may be stalling, despite the Fed keeping interest rates at a two-decade high.

April 10

-

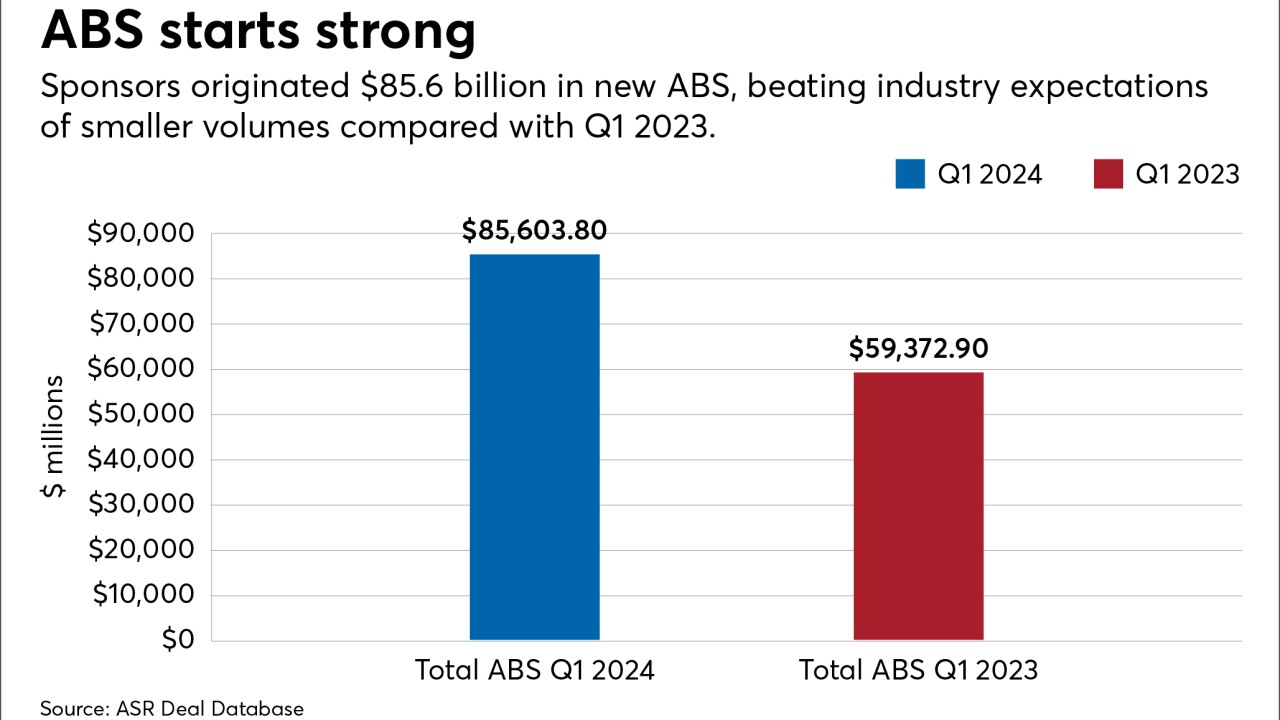

New originations exceeded last year's tally by 30.5%, despite concerns about how rates might impact consumer financial strength. Auto ABS production revved up overall performance.

April 9

-

Aside from overcollateralization and subordination, the notes get support from a reserve account representing 0.96% of the pool and an incremental reserve account maintain 1.00%.

April 9

-

Biden's "Plan B" would see loans reduced or wiped out for millions of Americans — including those whose debt exceeds their original principal amount.

April 8

-

Series 2024-2 can be upsized to $1.5 billion from the base pool amount, but regardless of the increase, pricing guidance, total credit enhancements and legal final maturities are expected to remain the same.

April 8

-

At the pool level, loans have a weighted average minimum liquid reserve of $5 million, and at the loan level the minimum for liquid reserves is $1 million for sponsors without a FICO score.

April 5

-

BJETS 2024-1 has leases and loans on 31 business jets in the collateral pool, 12 from Gulfstream and 11 from Bombardier, the two largest contributors.

April 4

-

He called the January and February inflation readings "a little bit concerning," and said he needs to see more progress on prices to gain confidence that they're moving toward the Fed's 2% target.

April 4

-

The Department of Housing and Urban Development agency warned in an online notice that issuers with prepayments exceeding certain limits could face sanctions.

April 4

April 4

-

Pricing ranges between 20 basis points, over the three-month Interpolated yield curve, on the A1 notes to 400 bps over the class E, at almost par, between 99.98% and 99.99%.

April 4

-

The four classes of notes are expected to price between 115 basis points on the class A notes to 415 bps on the class D, putting them virtually at par.

April 3

-

The deal will have a four-month prefunding period, and during that time the originators can originate and sell up to $13.6 million of additional contracts.

April 3

-

One tranche in the deal, supported by a pool of private student loans, matures every year beginning on June 1, 2029.

April 2

-

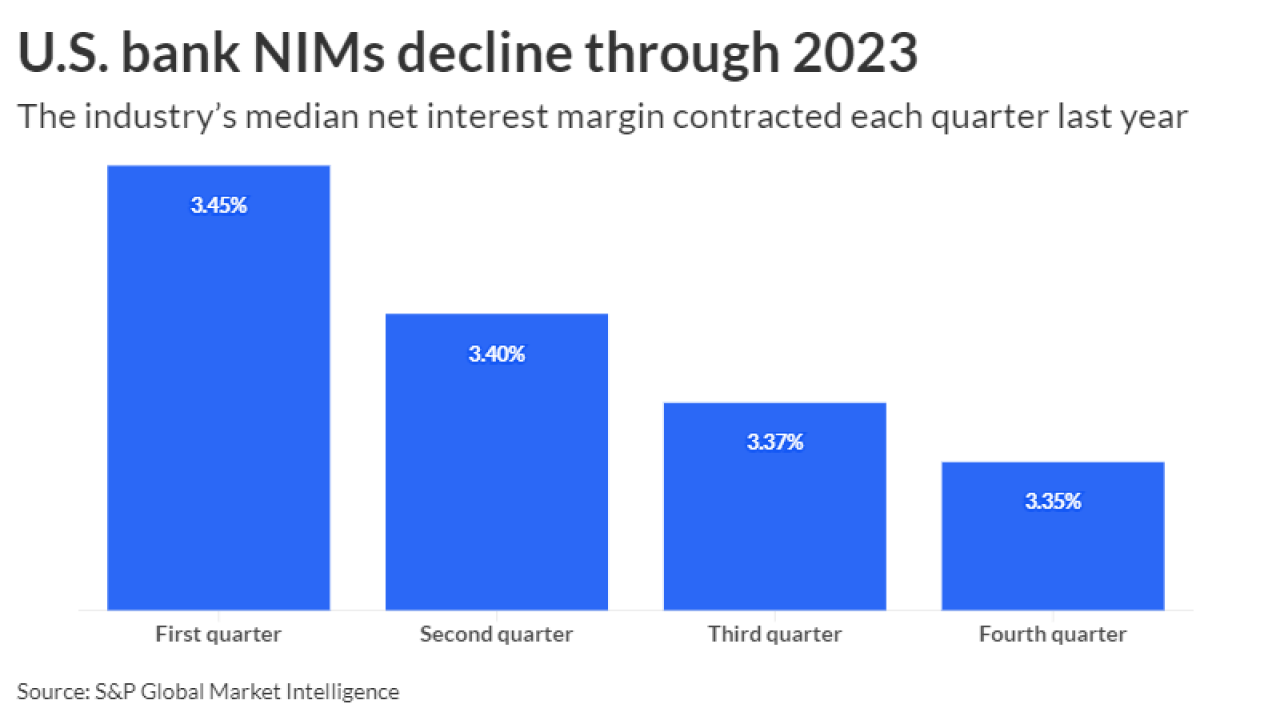

With high deposit and borrowing costs persisting amid the Federal Reserve's campaign against inflation, lenders face stress on their net interest margins and the potential of troubled loans ticking up.

April 2

-

The underlying loans have a (WA) FICO score of 734 across the statistical pool on the current deal, after coming in at 729 score seen on the previous deal, the HINNT 2022-A.

April 1

-

Powell reiterated it won't be appropriate to lower rates until officials are sure inflation is on track toward 2%, the rate they see as appropriate for a healthy economy.

March 30