Donna M. Mitchell is a financial journalist based in the New York metro area with expertise covering structured finance, commercial real estate, and wealth management. Her work has appeared in Forbes, Next Avenue, Financial Planning and National Real Estate Investor.

-

The notes will price against Treasurys, with spreads expected to fall between 85 and 90 basis points over the benchmark.

April 24 -

Bluegreen Vacation originated the loans and Fitch expressed confidence in its record of good performance as servicer.

April 23 -

Lendbuzz sells the notes as it juggles mixed performance results from 2023. Originations and revenues saw huge jumps, but so did operating expenses.

April 23 -

Price guidance was not available on the series 2024-1, the database notes that the series 2024-2 class A notes are expected to price between 63 and 65 basis points over the three-month interpolated yield curve.

April 22 -

With a high proportion of fixed-rate, interest-only underlying loans, the notes have almost no amortization, and three CRE loans have standalone, investment-grade opinions.

April 19 -

The fixed-rate loans are divided into three sub-pools that relied on rating methods from the RMBS, CMBS and ABS sectors to assess their risks.

April 18 -

The portfolio does not have any meaningful originations that have completed a full repayment cycle, making the company's performance data thin.

April 18 -

Formerly of Wells Fargo, she will coordinate several key units to create a structure for a sustained capital markets program that capitalizes on recent innovation and growth in home equity finance.

April 17 -

The Structured Finance Association questions whether funding closed-end seconds is an appropriate role for the government-sponsored enterprise, while newer lenders welcome the liquidity support.

April 17 -

The bank is a top auto lender, with a managed portfolio of $7.1 million through December 2023, and has a strong servicing track record.

April 17 -

ADMT 2024-NQM2 will repay senior position investors on a pro-rata basis, while the mezzanine and subordinate notes will be repaid sequentially.

April 16 -

That the underlying contract holders prioritize using their smartphones and other mobile devices suggests that they are likely to prioritize payments related to those products.

April 15 -

The current levels of credit enhancement are a reduction from levels of 58.0%, 48.7%, 35.9%, 22.5% and 17% on the classes A, B, C, D and E on the BLAST 2024-1 deal.

April 12 -

Most of the notes will be fixed rate, but the A1B tranche could be benchmarked to the three-month Secured Overnight Financing Rate (SOFR).

April 11 -

Griffin was a managing director at J.P.Morgan Securities, where he ran the global primary collateralized loan obligation (CLO) business.

April 11 -

A pool of open-end vehicle fleet lease and loan contracts for cars, trucks and other vehicles provide the revenues to the bonds.

April 11 -

There are four risk events that could stop cash flow into SMB 2024-R1's deal—missing overcollateralization targets, a stymied principal distribution and the deals do not exercise an optional clean-up call.

April 10 -

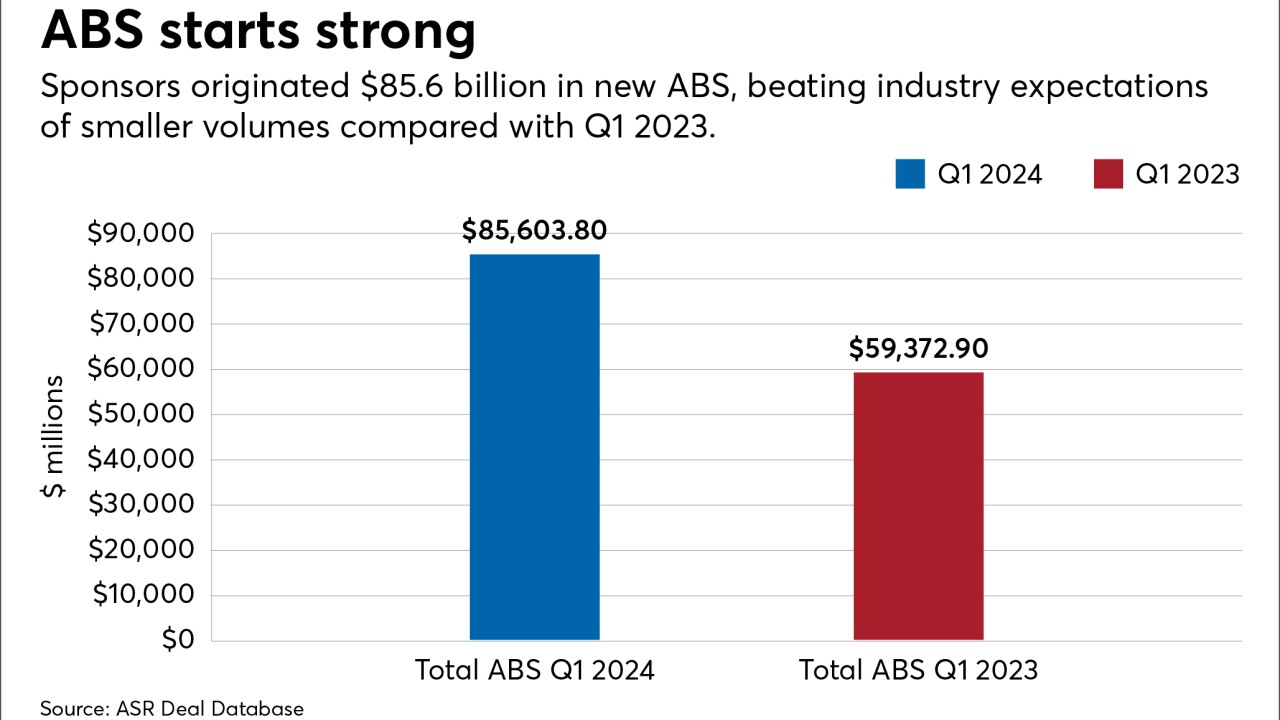

New originations exceeded last year's tally by 30.5%, despite concerns about how rates might impact consumer financial strength. Auto ABS production revved up overall performance.

April 9 -

Aside from overcollateralization and subordination, the notes get support from a reserve account representing 0.96% of the pool and an incremental reserve account maintain 1.00%.

April 9 -

Series 2024-2 can be upsized to $1.5 billion from the base pool amount, but regardless of the increase, pricing guidance, total credit enhancements and legal final maturities are expected to remain the same.

April 8