CLO securities pay out interest pegged to the three-month London interbank offered rate, but loans used as collateral are increasingly switching to one-month Libor and the spread between the two benchmarks has widened significantly.

-

Evan as the broader securitization market takes a breather, unusual deals from off-the-run asset classes continue provide diversification – and the opportunity to pick up yield.

July 16

July 16

-

The private equity firm recently obtained a $415 million first mortgage from Barclays and Morgan Stanley; proceeds, along with $125 million of mezzanine loans, will be used to repay existing debt of $512 million that was securitized in two prior deals.

July 16

-

The U.S. captive finance arms of Nissan North America and Daimler AG (Mercedes-Benz) have joined CarMax in sponsoring prime-loan asset-backed portfolios adding to a deal spree totaling $61.3 billion so far in 2018.

July 15

-

The 1,210-loans backing Gemgarto 2018-1 all finance owner-occupied loans, and none rely on self-certified or "fast-track" loans, according to presale reports from Moody's Investors Service and DBRS.

July 15

-

The collateral includes both QM and non-QM loans; however, certain loans are designated as QM even though the borrower’s DTI may be above 43%, due to a temporary exemption for GSE-eligible loans.

July 13

-

The Dallas-based lender's third foray into the deep subprime ABS market in 2018 arrives as recent Santander DRIVE securitizations are performing well with recently lowered loss expectations from S&P Global Ratings.

July 12

-

New collateral can be added to the $824.2M Ford Credit Auto Owner Trust REV 2018-2 until 2023; that's two years less than the revolving period on its prior deal, completed in January.

July 12

-

Fannie Mae and Freddie Mac may need to tap into U.S. Treasury funds when they adopt CECL, a new accounting rule that makes companies set aside money upfront for expected loan losses.

July 12

July 12

-

The €414.2 million CVC Cordatus Loan Fund XI will issue exchangeable shares for four classes of notes; this allows the fund to hold bonds without putting itself off-limits to U.S. banks.

July 12

-

In the U.S., the 12-month trailing default rate fell to 3.4% in June from 4% in March, while in Europe it declined to 2.2% from 2.8% over the quarter. Globally, defaults stood at 2.9%, down from 3.4% in the first quarter.

July 11

-

The $450 million Thunderbolt II Aircraft Lease transaction involves 18 aircraft representing the younger planes in Air Lease's $13 billion portfolio of owned and managed passenger jets.

July 11

-

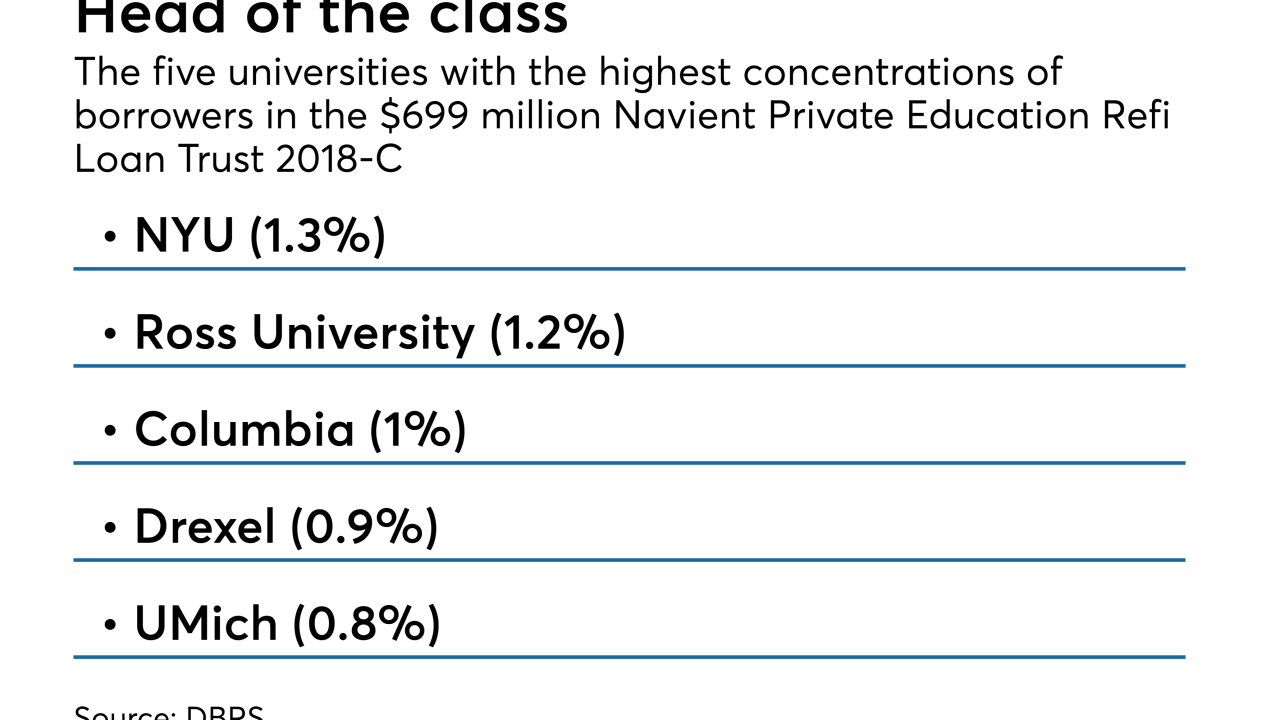

Just 66% of the collateral Navient Private Education Refi Loan Trust 2018-C consists of loans to borrowers with graduate, medical, law or other advanced degrees, down from 72% in a similar transaction in February.

July 11