-

Meanwhile, the average new-home mortgage price climbed to a new all-time high, according to the Mortgage Bankers Association.

July 20

-

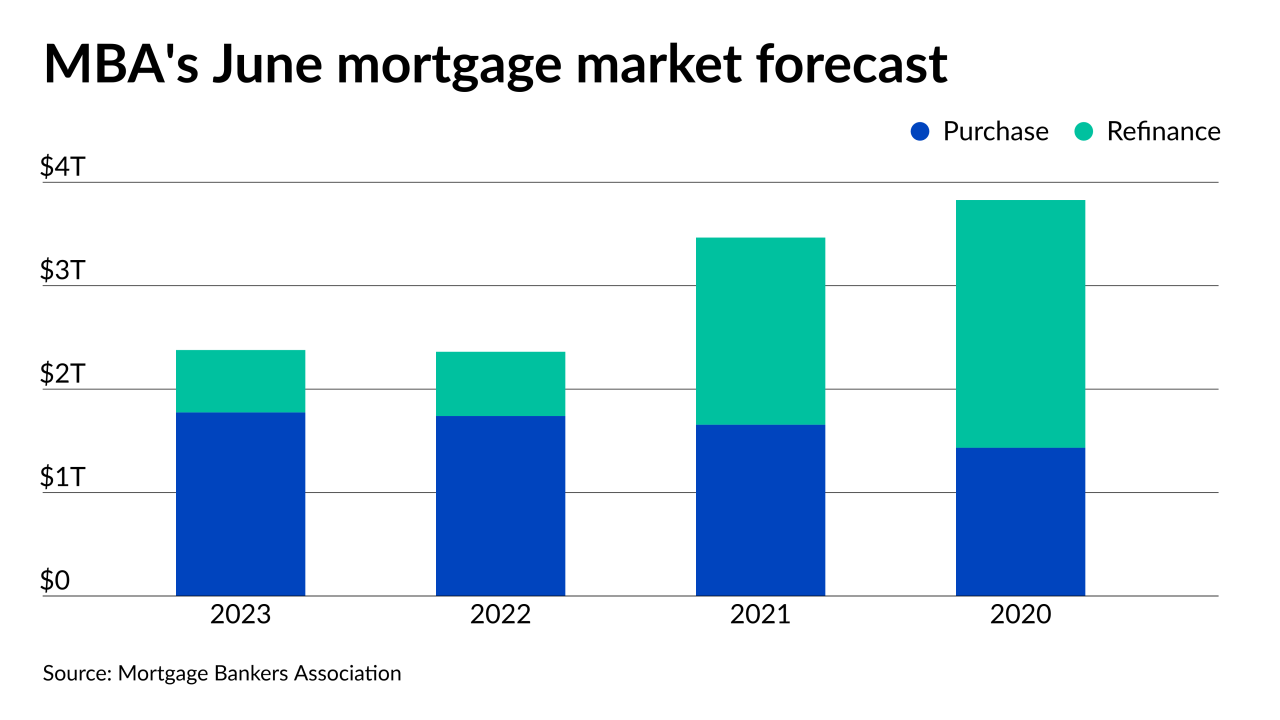

The GSE forecasts $4 trillion in production this year because refinance activity is stronger than expected.

July 16

-

The agency’s new chief said eliminating the “adverse market fee” — in place since December — will make it easier for families to refinance while mortgage rates are still low.

July 16

-

The return of more normalized numbers for two key players in the home loan market could be the lead-up to a wave that’s been anticipated since the coronavirus arrived.

July 14

-

Income share agreements, which allow college graduates to repay tuition financing as a percentage of their future income, have come under fire lately from consumer advocates for questionable marketing and other potential legal violations. Some hope a partnership between a Virginia bank and an ISA provider will give the product more legitimacy, while others worry it just masks risks for borrowers.

July 12

-

The change makes it easier for borrowers exiting forbearance to get access to home retention options that might otherwise be out of reach due to skyrocketing home prices.

June 30

-

The lack of homes for sale is supporting the record values, unlike what happened in the mid-2000s, analysts say.

June 28

-

The Supreme Court decision cleared the way for further revisions to the agreements between the Federal Housing Finance Agency and the Treasury, which could include dismissing the January changes.

June 25 -

The Community Home Lenders Association has called for suspension of federal limits on the loan volumes that Fannie Mae and Freddie Mac can purchase from individual lenders. The demand came on the same day that the Biden administration fired FHFA Director Mark Calabria and started the process of nominating his successor.

June 24

-

Growing CRE mortgage volumes raised the bar for the coming year despite lingering concerns, according to the CRE Finance Council.

June 23

-

President Biden removed Mark Calabria as Federal Housing Finance Agency director hours after a Supreme Court ruling made the move possible. The administration is expected to offer up a nominee who will prioritize affordable housing and racial equity in housing instead of reforming Fannie Mae and Freddie Mac.

June 23

-

The fintech specializes in lending to dentists, veterinarians and other solo providers looking to grow or establish their own practice.

June 22

-

Cannabis, though still illegal at the federal level, continues to inch into the financial mainstream. Small credit unions and lenders as large as Valley National and East West have moved beyond just taking deposits from marijuana companies.

June 21

-

The housing starts and permit data suggest the pace of residential construction may be moderating after a recent run-up in building-materials costs.

June 16

-

More than two-thirds surveyed said they expect to make less money over the next three months as price reductions ramp up along with a market shift to purchases.

June 10

-

Most of the coal plants that feed the biggest U.S. power grid will soon no longer be economic to run after prices in a key auction plunged to the lowest in 11 years.

June 8

-

The deal for the Salt Lake City-based home improvement lender, which Home Depot tried to acquire more than a decade ago, is part of a larger effort by Regions Financial to diversify its home lending business.

June 8

-

For two decades, Alfred Pollard served as the general counsel for Fannie Mae and Freddie Mac’s regulator. He had a front-row seat for the establishment of the Federal Housing Finance Agency, the government’s subsequent seizure of the mortgage giants amid mounting losses in 2008 and the more recent legal dispute over the FHFA’s authority.

June 7

-

DeVito takes over on June 1, replacing interim CEO Mark Grier, who returns to his seat on the government-sponsored agency's board.

May 26

-

The deal is the second securitized transaction floated under recent California state legislation authorizing a flurry of utility securitizations.

May 21