-

Federal Reserve watchers expect a board of governors vote in February to reappoint the 12 regional Fed bank presidents — which is typically treated as a formality — to be the next flashpoint in the White House's effort to bring the central bank to heel.

December 8

December 8

-

Merchant's notes have several key credit strengths, including that vehicle fleet lease securitization pools have had very low delinquencies and losses historically.

December 5

December 5

-

No subordinate notes—the class M notes, essentially—will receive any principal payments until the senior class A notes have been paid down to zero.

December 5

-

Enpal issues the first European public securitization for heat pumps and solar panels.

December 4

-

Delinquency trends split in Q3, with securitized and agency loans showing more strain while banks and life companies saw small improvements amid uneven vacancy and rent conditions.

December 4

December 4

-

Levkowitz is known in the capital markets for founding Signal Hill Holdings, and as managing partner of Penn Properties, a real estate investment firm.

December 4

-

The European Banking Federation and the Association for Financial Markets in Europe said the planned tweaks risk "curtailing the utility of securitization."

December 4

-

After the prefunding period, up to 7.50% of the total pool balance will consist of collateral from earlier transactions or newly acquired assets, timeshare loans.

December 3

-

New securitization volume should surpass 2024 business by 16%, after getting a boost from consumer asset-backed securities (ABS) classes and do $948 billion in new business in 2026.

December 3 -

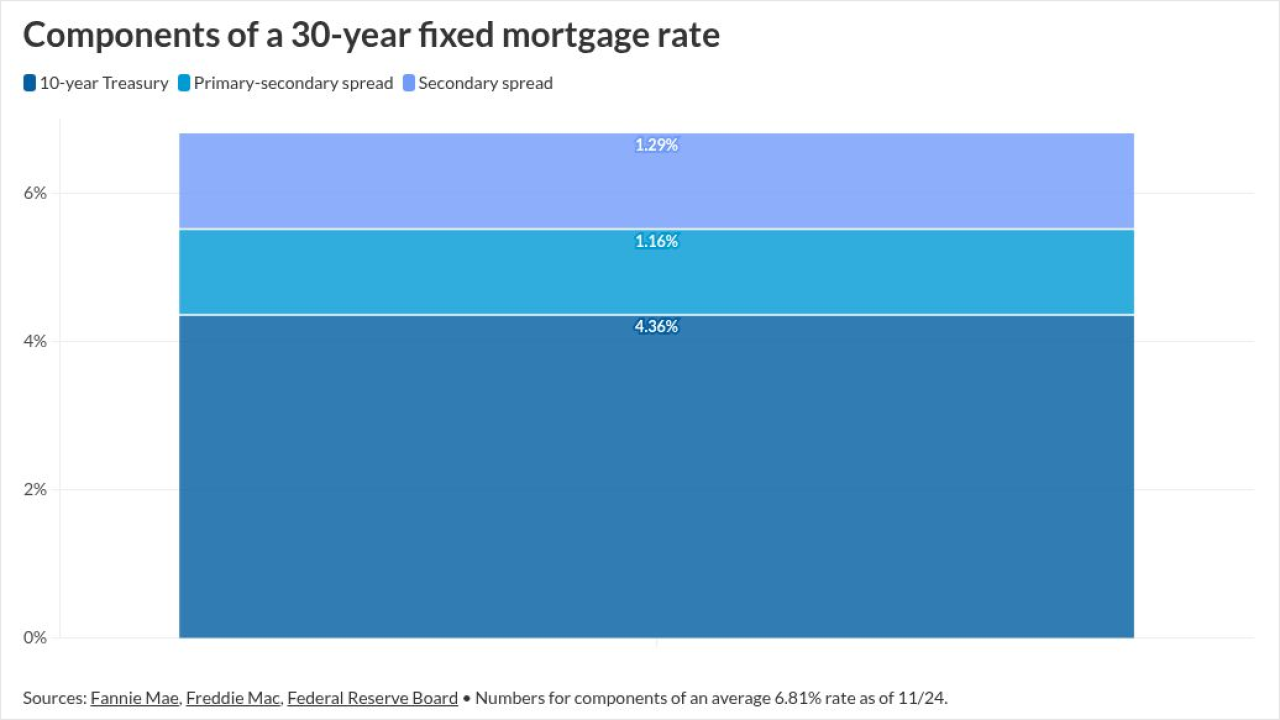

At issue is the CFPB's weekly publication of Average Prime Offer Rate tables, a key benchmark enabling the smooth operation of the $13 trillion residential mortgage market.

December 3

-

Decision makers have voiced support for lower financing costs but researchers have said achieving it could be complicated. Part 3 in a series.

December 3

December 3

-

BRAVO Residential Funding's notes will repay investors through a sequential payment structure, and include a step-up coupon for classes A-1A, A-1B, A-2 and A3.

December 2

-

What developments around rent reporting and new credit standards portend for mortgage companies. Part 2 of a series on government-sponsored enterprise changes.

December 2

-

The underlying portfolio consists of 608,810 contracts, with two thirds of the cash flow supporting the transaction from a wholesale agreement that includes T-Mobile.

December 1

-

If cumulative loss or a delinquency trigger event is in effect, then the deal will distribute principal among the class A notes before any principal allocation the class M1 or class B certificates.

November 26

-

Baby Boomers' annuities purchases continue to fuel banks' lending to collateralized loan obligations, asset-backed securities and special purpose entities.

November 26

-

For TIP Solar ABS, the securitization share of ADSAB and cashflows payable to the cash equity holder, are about $200 million and $171.4 million.

November 25

-

Denmark has offered additional checks and balances by the European Systemic Risk Board as a way to address concerns that insurers' investment in synthetic risk transfers could threaten financial stability.

November 25

-

There is also a class N tranche of notes that make payment to those noteholders if funds are available after the overcollateralization.

November 24

-

The transaction uses a shifting interest repayment structure, and its lockout that is subject to performance triggers.

November 24