-

The deal features a principal acceleration trigger. If breached, the transaction will divert all additional funds to paying down the principal on the notes.

May 7

May 7

-

The transaction comes to market with initial hard credit enhancement levels of 33.60%, 22.90%, 13.50% and 8.65% across the subordinate tranches, higher than the previous deal.

May 7

-

The A1 VFN tranche is a variable funding note whose proceeds can be used for general corporate purposes, including acquisitions.

May 6

-

An array of unnamed originators accounted for the large majority of originators in the pool, 89.3%, the rating agencies said, while Hometown Equity Mortgage originated 10.7% of the pool.

May 5

-

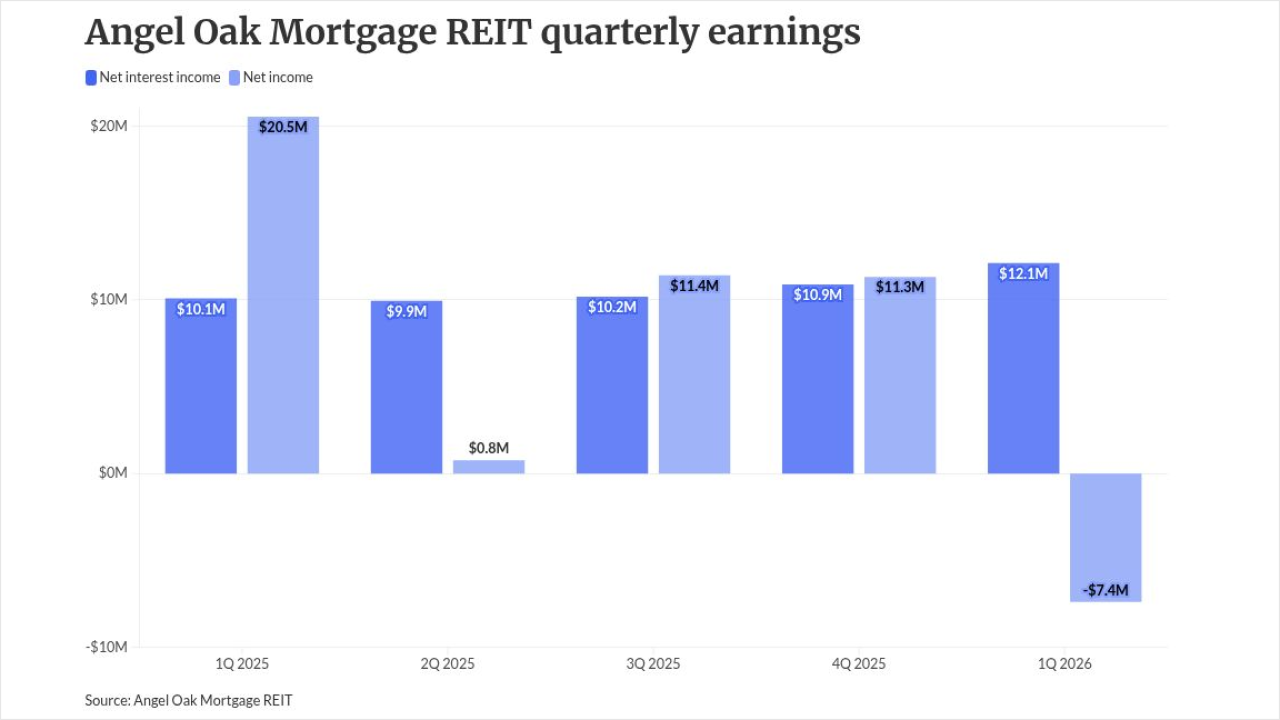

Economic uncertainty weighed on risk appetite, but the current performance of the non-QM market is "durable," Angel Oak leaders said in an earnings call.

May 5

May 5

-

Kapitus funds receivables through two revolving securitizations totaling $575 million, and a $230.1 million warehouse line of credit from Truist, which matures in June 2027.

May 5

-

PRET 2026-RPL2 uses a sequential repayment structure, although the notes will not advance any principal and interest from delinquent loans.

May 4

-

Borrowers in the pool had a non-zero weighted average credit score of 608, with a 112.12% loan-to-value (LTV) ratio.

May 1

-

The notes are expected to pay coupons including 5.00% on the A6 through A30 tranches of notes, and 6.13% on the B1 through B6 notes.

April 30

-

The weighted average, base-case annualized gross loss declined from 11.78%, from 11.86%, because of minor changes in its assumptions of pool segment defaults.

April 29

-

The whole business deal, built around a master trust structure, will be repaid primarily from franchise royalty revenue.

April 29

-

The three class A notes, A1, A2 and A3, of GCAR 2026-2 notes will all benefit from hard credit enhancement levels, plus haircut to excess spread of 56.07%.

April 28

-

Irrespective of the transaction's trigger status, PRKCM 2026-AFC3 will pay the A-1FCF first, until its balance is reduced to zero, and then to the A-1LCF until it is paid down.

April 28

-

Bank statement underwriting, often applied in situations where the borrower is self-employed, accounted for the plurality of documentation types in the pool, at 44.9%.

April 27

-

The deal saw notable changes from SCLP 2021-1, especially an increase in target and initial overcollateralization.

April 27

-

Tower Point Capital, the deal's manager, is considered to have one of the largest privately held wireless infrastructure portfolios in the U.S.

April 24

-

Non-qualified loans are the majority of loans in the pool, 59.2%, while loans exempt from the Ability-to-Repay/Qualified Mortgage rule, represent 35.9%.

April 23

-

February's securitization from Vertical Bridge was the sector's largest-ever deal and included the sector's first single-B rated tranche.

April 23

-

Any additional securities that the transaction issues will rank equally with the class that has the same class designation.

April 21

-

Initially, the transaction will follow a sequential repayment structure that requires each note class to reach a required overcollateralization percentage before the next subordinate class begins receiving principal.

April 21